Compare the ending balance of your accounting records to your bank statement to see if both cash balances match. Before you reconcile your bank account, you’ll need to ensure that you’ve recorded all transactions from your business until the date of your bank statement. If you have access to online what is bookkeeping banking, you can download the bank statements when conducting a bank reconciliation at regular intervals rather than manually entering the information.

Bank Fees

If you’re not careful, your business checking account could be subject to overdraft fees. In order to prepare a bank reconciliation statement, you’ll need to obtain both the current and the previous month’s bank statements as well as the cash book. NSF checks are an item to be reconciled when preparing the bank reconciliation statement, because when you deposit a check, often it has already been cleared by the bank.

Nowadays, many companies use specialized accounting software in bank reconciliation to reduce the amount of work and adjustments required and to enable real-time updates. Keeping on top of your bank reconciliation ensures that you’re always aware of your company’s financial situation. This helps you anticipate any cash flow challenges so you can respond appropriately.

Reconcile Balances

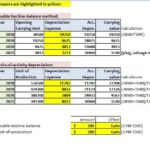

As a result, your balance as per the passbook would be less than the balance as per the cash book. In this instance, your bank has recorded the receipts in your business account at the bank, while you haven’t recorded this transaction in your cash book. As a result, the balance shown in the bank passbook would be more than the balance shown in your company’s cash book. When your business receives checks from its customers, these amounts are recorded immediately on the debit side of the cash book so the balance as per the cash book increases.

Consider performing this monthly task shortly after your bank statement arrives so you can manage any errors or improper transactions as quickly as possible. Income from variable sources like interest and investment may be difficult to predict. As such, exact amounts may not be accurately included on financial statements before the reconciliation process. When the business receives its bank statement, it can use the final amounts of interest and investment income to make adjustments and reconcile its financial statements. Conducting regular bank reconciliation helps you catch any fraud risks or financial errors before they become a larger problem. This includes what are the types of internal controls everything from major fraud and theft to accounting miscalculations, insufficient funds, and incomplete or duplicated payments.

The Future of Bank Reconciliations

- However, you typically only have a limited period, such as 30 days from the statement date, to catch and request correction of errors.

- Bank reconciliation accounting is performed by the accounts payable department.

- Keeping accurate records of your bank transactions can help you determine your financial health and avoid costly fees.

- When your balance as per the cash book does not match with your balance as per the passbook, there are certain adjustments that you have to make in order to balance the two accounts.

We’ll take bookkeeping completely off your hands (and deal with the bank reconciliations too). You can do a bank reconciliation when you receive your statement at the end of the month or using your online banking data. Reconciling your bank statements won’t stop fraud, but it will let you know when it’s happened. Reconciling bank statements typically happens at the end of each month when your financial institution sends over your statement. If you find any bank adjustments, record them in your personal records and adjust the balance accordingly. If you’ve been charged a fee in error, contact your bank to resolve the issue.

Step 1: Match Each Item on the Bank Statement to the Cash Account

Standardizing the process with a set of steps to follow for reconciliation can make the process more organized and save time. This can be done by creating a checklist or using a reconciliation software tool. Some businesses, which have money entering and leaving their accounts multiple times every day, will reconcile on a daily basis. There’s nothing harmful about outstanding checks/withdrawals or outstanding deposits/receipts, so long as you keep track of them. Small business owners may find that sufficient funds from the previous month what does it mean to be in the black or in the red are not enough.

Depending on how you choose to receive notifications from your bank, you may receive email or text alerts for successful deposits into your account. Whatever method you prefer, it’s important to keep solid records of every transaction to reconcile your bank account properly. To do this, businesses need to take into account bank charges, NSF checks, and errors in accounting.